What “blacklisted” really means for South Africans

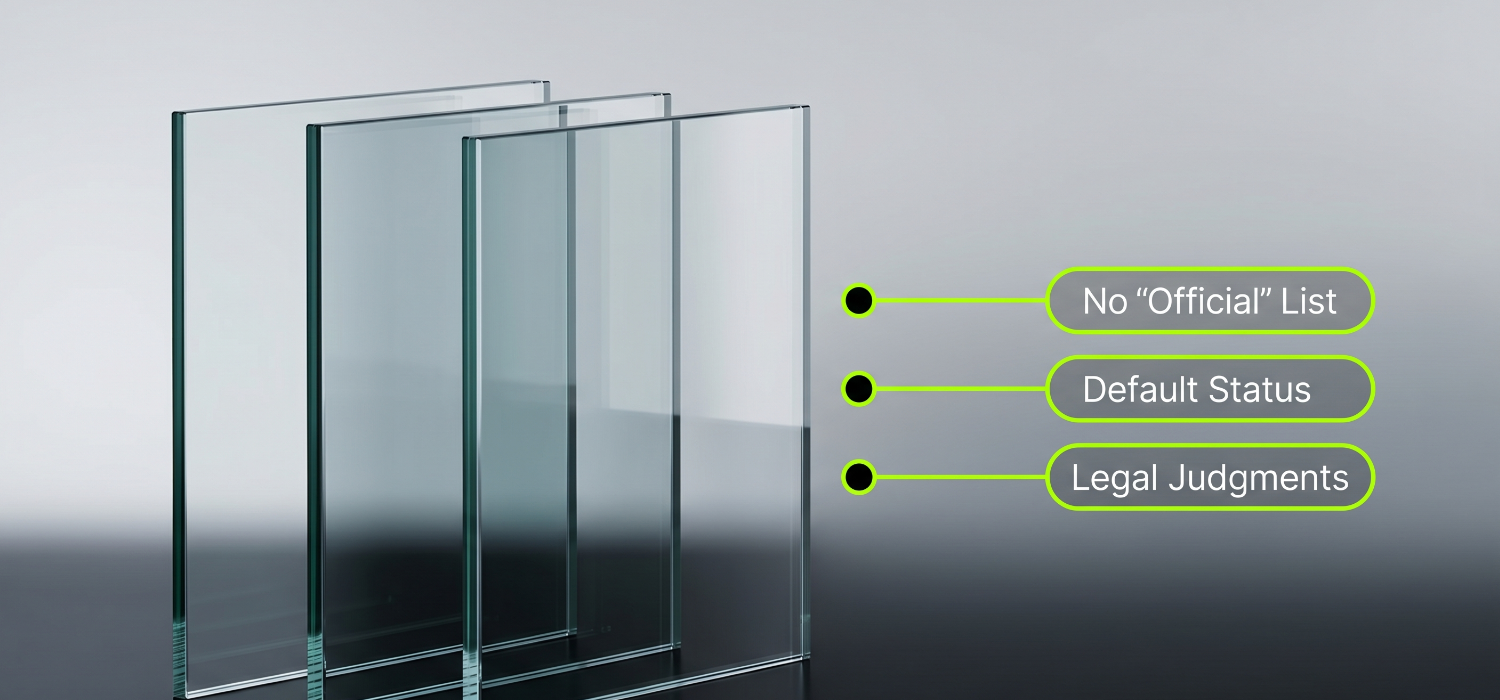

Many South Africans still use the word “blacklisted”. But there is no official blacklist anymore.

What people usually mean is there is negative information on their credit report, like missed payments, accounts in default or a judgment. And this kind of information can affect whether a lender approves you for credit.

So, if you are wanting to check if you are “blacklisted” in South Africa, the answer is this: you need to check your credit report and credit score.

It’s the clearest way to see your credit blacklist status and understand what credit providers may be seeing.

Checking for any credit report errors is the key and Finance365 is a useful place to start because it helps you see your credit information in one place.

You can get your latest credit report from us here.

When you check your report, look for:

- Accounts shown as overdue or in default

- Judgments or legal listings

- Accounts you do not recognise

- Balances or payment statuses that look wrong

- Information that should already have been updated or removed

5 key indicators that may tell you there is a problem

You cannot know for sure just by guessing, but these warning signs often point to trouble on your credit profile:

- You have missed payments for a while: If you have fallen behind on accounts, they may be listed as overdue or in default on your report.

- Your credit applications keep getting declined: If you are turned down for a loan, store account, cellphone contract or other credit, negative information may be affecting the decision.

- You are approved, but for less than expected: A smaller limit or stricter terms can be a sign that a lender sees you as higher risk.

- Debt collectors are contacting you: Calls, letters, emails or messages from collectors can mean an unpaid account has already moved into a more serious stage.

- You have had legal action taken against you: If a court judgment has been granted, it may appear on your credit report.

How to get off the “blacklist”

It comes back to this. If you want to check if you are blacklisted South Africa, do not rely on rumours or old ideas. Check your credit report.

You can also dispute incorrect information if you spot a problem. The National Credit Regulator says consumers should review their reports and challenge any errors.

That last point matters. As credit report errors do happen and they can hurt your chances of getting approved.

Also know that not all negative listings stay there for the same amount of time.

Under South African credit regulations, some information can stay on a report for limited periods, depending on the type of listing.

Judgments can stay for up to thirty years unless lifted earlier, while some other adverse information is kept for shorter periods.

That is why checking matters. You need to see what is there, whether it is correct, and whether it should still be there.

What to do next if you find a problem

Start by checking whether the listing is correct. If it is wrong, dispute it with the credit bureau that issued your latest credit report.

If the debt is real, don’t wait. Contact the credit provider and make a payment arrangement. You may not fix everything overnight, but paying on time and reducing overdue debt can help your credit profile recover over time.

Last but not least, work with facts, not out of fear of the unknown

Just hearing the term “blacklist” linked to your credit record may still cause you worry, but the important thing is to deal with the facts.

The sooner you check your report, the sooner you can spot problems, correct mistakes, and take steps to improve your position. In every case, knowing where you stand is the first step to being in control of your finances.