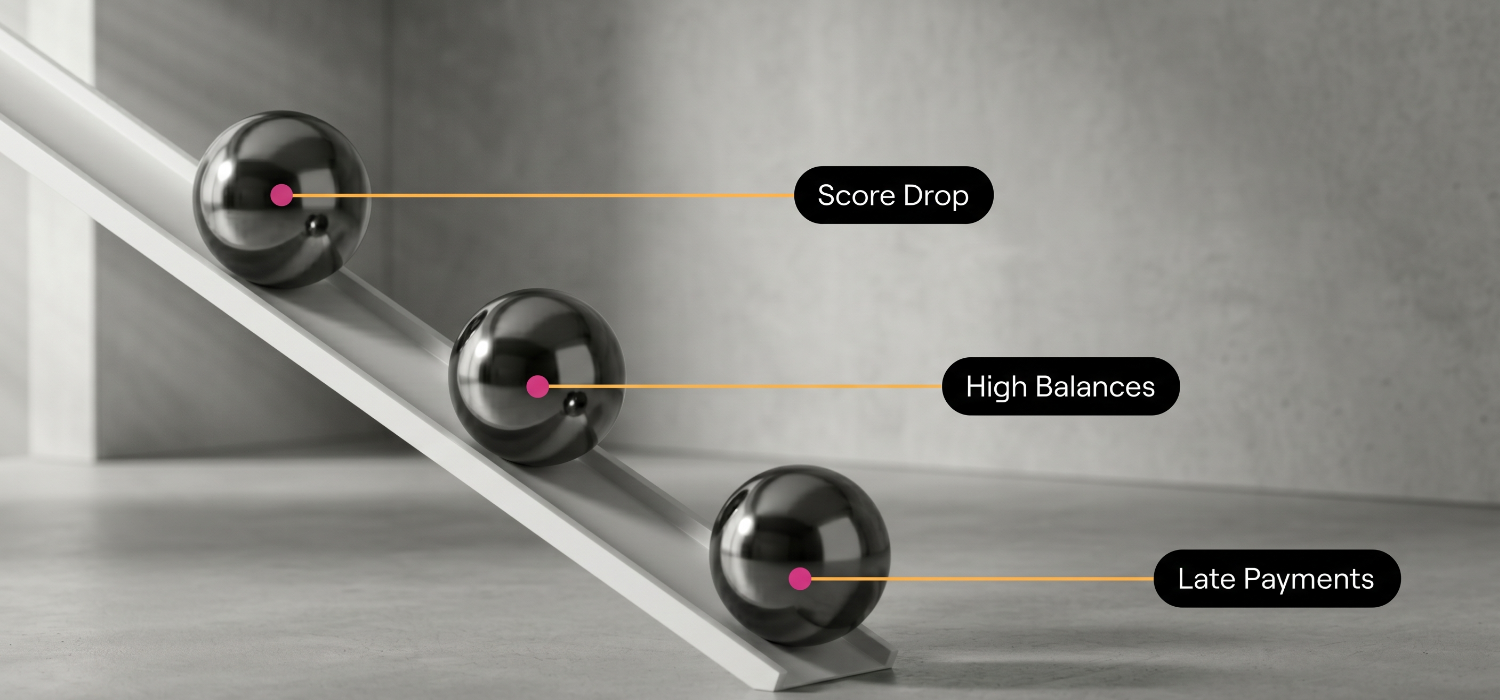

6 reasons for a drop in your score

There are times in the year when people mentally “switch off” a little financially.

In South Africa, that’s often during school holidays, December, or long public holiday weekends where one day off somehow turns into four. People travel. Rest. Spend more.

That’s usually when checking your credit score becomes the last thing on your mind. But then normal life starts again and suddenly your score has dropped, or a credit application gets declined out of nowhere.

That’s when many people ask: “Why is my credit rating low?”

The important thing to know is that credit scores can shift quietly in the background while life is happening. Missed payments, higher balances after holiday spending, too many credit applications, or even admin mistakes can all affect your profile.

But remember that a lower score does not always mean financial disaster. It usually means it is time to understand what affects your credit score and what steps you can take next.

Here are 6 common reasons for low credit score problems in South Africa:

1. Paying late or missing payments

This is one of the biggest reasons for low credit score problems. Even small late payments can affect your profile over time.

Your payment history tells lenders how reliable you are with credit.

2. Using too much of your available credit

If your accounts are always close to their limits, lenders may see this as financial pressure.

For example, if your credit card limit is R10 000 and your balance regularly sits near R9 000, it can negatively affect your “credit score South Africa” profile.

3. Applying for lots of credit close together

Multiple applications in a short period can make it look like you are desperate for credit, even if that is not true.

This is why applying everywhere after one rejection can sometimes lower your score even further.

4. A very short credit history

Young adults or people new to credit may have lower scores simply because they do not have enough borrowing history yet.

This does not mean you are bad with money. It simply means there is less information available about your payment behaviour.

5. Defaults, judgments or debt review

Serious payment problems can lower your score significantly.

Some people still call this being “blacklisted”, but there is no official blacklist in South Africa anymore. Instead, lenders look at negative information listed on your credit report.

6. Mistakes on your credit report

Sometimes the problem is not your spending. It is admin.

An account could still show unpaid after being settled. A balance may be incorrect or there may be a credit check you do not recognise. That is why regular credit monitoring makes a difference.

How to fix a low credit rating

The first thing not to do is panic. The second thing not to do is apply for more credit everywhere.

Instead:

- Check your credit report carefully

- Look for balances or accounts that seem wrong

- Dispute any errors you find

- Catch up missed payments where possible

- Reduce balances on heavily used accounts

- Avoid unnecessary new credit applications

- Speak to creditors early if you are struggling financially

Often, the biggest improvement starts with understanding what is pulling your score down.

Improving your score usually takes time. But steady habits matter. Paying on time consistently, lowering debt, and managing credit carefully all help rebuild trust in your profile over time.

Importantly, checking your own score does not lower it. In fact, regular monitoring is one of the best things you can do because it helps you spot problems early and track your progress properly.

Your next move matters more than your last few months

Checking your credit report regularly helps you stay closer to what is happening financially while life keeps moving around you. It helps you spot problems early, understand your profile better, and make calmer decisions before applying for credit again.